After China's accession to the WTO, the assets of the auto parts industry rose year by year, accounting for the proportion of the total assets of the entire automobile industry, jumping from about 5% in 2002 to about 35% in 2006. At present, the automobile industry has increasingly become an important pillar industry in China's national economy. The auto parts industry is the upstream industry in the entire automobile industry. It occupies an increasingly important position in the entire automobile industry chain.

With the national auto industry starting to emerge from the slow-moving state since the second half of 2004, the auto parts industry has also begun to warm up overall, demand has been stimulated, and the market has maintained a good growth. National Bureau of Statistics data show that in 2006 China's auto parts industry completed industrial output value of 539.705 billion yuan, an increase of 34.35% compared with the previous year; auto parts products sales revenue 527.235 billion yuan, an increase of 34.71%. The annual import value of auto parts products was 12.459 billion US dollars, an increase of 34.18% over the previous year; the export value was 210.72 billion US dollars, an increase of 38.21% over the previous year.

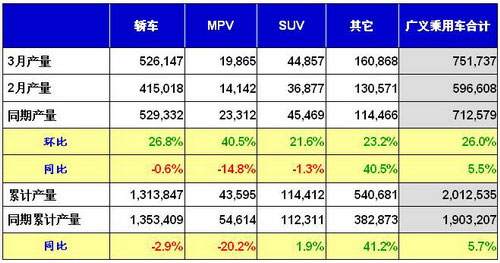

March production analysis table

March production analysis table In recent years, the rapid development of China's automobile industry has resulted in the production and supporting systems of various types and entire series of complete vehicles and components. The industrial concentration has been continuously improved, and the level of product technology has been significantly improved. It has become a world leader in automobile production. However, problems such as irrational industrial structure, low technical level, weak self-development capabilities, and imperfect consumer policies are still prominent, and constraints such as energy, environmental protection, and urban transportation are increasingly evident. Since the second half of 2008, with the spread of the international financial crisis and the serious shrinkage of the international auto market, the domestic auto market has been severely impacted, resulting in negative growth in the production and sales of the entire industry, the economic benefits of key enterprises, and the lack of development of self-owned brand cars. The situation of industrial development is grim.

Fortunately, from the end of 2008 to the end of the year, with the economic crisis spreading across the globe, the Chinese market has increasingly become the focus of global attention. Its huge consumption potential and good development characterization have become attractive to many domestic and foreign automotive and parts companies. The important factor of investment. China Automobile Association expects that the total automobile sales in 2009 will exceed 10 million for the first time, reaching 10.2 million units, an increase of 8.7% over the previous year. Passenger car sales reached 7.45 million, an increase of 10.2% year-on-year, and commercial vehicles sales were 2.75 million, an increase of 5% year-on-year.

1, political environment

After years of rapid growth, the automotive industry is bound to undergo a major adjustment to resolve many contradictions in the internal structure and external environment. The international financial crisis has only triggered the early arrival of the structural adjustment period. At present, China's auto market is in a period of growth. The market demand for urban and rural markets is huge, and the fundamentals for the development of the auto industry have not changed. In order to actively respond to the international financial crisis and maintain stable and rapid economic development, we must accelerate the adjustment and revitalization of the automobile industry.

In March 2009, the government formally launched the "Auto Industry Adjustment and Rejuvenation Plan." The auto industry is an important pillar industry of the national economy. It has a long industry chain, a high degree of correlation, a wide range of jobs, and a large consumer pull. It is in the national economy and social development. Play an important role.

In response to the impact of the international financial crisis, we will implement the overall requirements of the Party Central Committee and the State Council to ensure growth, expand domestic demand, and adjust structure, stabilize automobile consumption, accelerate structural adjustment, enhance independent innovation capabilities, promote industrial upgrading, and promote the sustainable, healthy, and sustainable development of China's auto industry. With stable development, this plan is specifically formulated as an action plan for the comprehensive response of the automotive industry. The planning period is 2009-2011.

[next]

2. Macroeconomic environment

Since the reform and opening up, China has achieved an average annual growth rate of 9.6% in the past 30 years with the world’s largest population size. Even with the global economy in crisis, China’s GDP reached a level in 2008. 3006.7 billion yuan, an increase of 9.0% over the previous year and a contribution to world economic growth of over 20%. Preliminary calculations show that in the first quarter of 2008, China’s GDP increased by 10.6% year-on-year, 10.1% in the second quarter, 9.0% in the third quarter, and 6.8% in the fourth quarter. In terms of sub-industries, the primary industry has an added value of 3.40 trillion yuan, an increase of 5.5%; the secondary industry has an increase of 146.183 billion yuan, an increase of 9.3%; the tertiary industry has an increase of 1.2 trillion yuan, an increase of 9.5%, which eliminates deflation. There is no obvious inflation, the quality of economic development is improved, benefits are improved, fluctuations are reduced, and coordination is enhanced.

Due to the slowdown in macroeconomic growth and large price increase, the growth rate of urban residents and rural residents' income will be significantly lower than in 2007. In 2008 and 2009, the actual per capita disposable income of urban residents will increase by 8.1% and 8.0% respectively. The actual per capita net income of rural residents will increase by 7.8% and 7.4% respectively. The gap between income growth of rural residents and urban residents has narrowed, but we need to continue to work hard to change the situation in which the growth rate of rural residents’ income is still lower than that of urban residents.

In recent years, China’s trade surplus and foreign exchange reserves have continued to grow at a rapid rate. Since 2008, under the influence of the US subprime mortgage crisis, weakening of international demand, the increase in the price of imported goods higher than the price increase of exports, and the appreciation of the renminbi, the import growth rate has increased significantly, the growth rate of exports has slowed down, and the trade surplus has begun to Fall back. It is expected that the growth rate of imports and exports in 2008 will reach the level of 28.9% and 22.2%, respectively, and the annual foreign trade surplus will be slightly lower than the previous year, reaching about 257 billion US dollars; the growth rate of imports and exports will reach 25.0 in 2009 respectively. At the level of about % and 20.2%, the trade surplus for the whole year will further drop to about 251 billion U.S. dollars.

In general, China's current macroeconomic fundamentals are still in good shape and will continue to maintain a steady and rapid growth. Although the economic growth rate has slowed down in 2008 and 2009, it is still reasonable. Within the range. On the other hand, we must pay close attention to the possible impact of the further evolution of various unfavorable factors in the international economic environment in the recent period. We must review the situation, continue to work hard on macroeconomic regulation and control, seize favorable opportunities, actively resolve negative factors, and strive to maintain sound and rapid economic development while deepening reforms and accelerating the transformation of economic development methods.

3, micro industry environment

China’s huge market potential and low labor force are attracting more and more multinational auto parts groups. According to statistics, of the more than 5,000 auto parts companies in China, more than 1,200 are foreign-invested companies, and most of them. It is a Fortune 500 company. China began to become a world auto parts production plant, and the market competition has intensified.

As the competition pressure of vehicle companies intensifies, the pressure of competition is also transmitted to parts and components companies. In order to solve the problems of scattered parts, chaotic parts, and poor economic returns of the parts and components industry, parts and components companies are required to reduce costs and make large-scale investments. It must rely on the strength of market economy and make full use of the effects of economies of scale. Therefore, in the future, the auto parts industry will be guided by macroeconomic policies and implement mergers and acquisitions with the same industry or mergers and acquisitions between different industries to maximize market maximization, maximize benefits, and minimize costs. The purpose of competing with foreign companies.

In the segmentation industry, engines, chassis, tires, automotive electronics and other industries have maintained a rapid development trend. From the perspective of the investment in component products, the overall flow of investment funds is mainly concentrated on the following major categories of system components: First, engine components. The company is dominated by engine assemblies, pistons, piston rings, and radiators. The capital flow is mainly concentrated on engine assemblies and EFI products. The second is chassis components. Gearboxes, gears, brake systems, and shock absorbers are the mainstays, with the capital flow of the chassis assembly being relatively high. The third is non-metallic parts such as rubber, tires, and plastics, as well as castings and forgings. Fourth, the body trim parts. Among them, the scale of investment in air conditioners and heaters, seats and recliners is relatively high. Fifth, automotive electrical parts and components.

In terms of industrial layout, China’s parts and components industry has formed five regions in the Bohai Rim region, the Yangtze River Delta region, the Pearl River Delta region, the Hubei region, and the central and western regions in terms of geographical distribution. As of the end of 2006, there were 6,142 auto parts companies in China. It is also basically concentrated in these regions, of which the largest number of enterprises in Zhejiang Province has a total of 1279 parts and components companies, accounting for 20.82% of the total number of enterprises in the country; the number of companies in the top six provinces are Zhejiang, Jiangsu, Shandong, Hubei, and Shanghai. In Guangdong, the number of enterprises in these six regions together accounted for 57.96% of the total number of enterprises in the country.

Although China's spare parts industry has made great progress in recent years, but from the perspective of the global market, China's spare parts industry is scattered, the degree of industrial concentration is not high, the vast majority of small-scale enterprises do not have sufficient operating funds, but also lack of research and development capabilities, It is impossible to develop advanced products that meet the needs of the market. These problems, such as inefficient structurality, have not only hindered the healthy development of China's parts and components industry, but also caused considerable restraints on the vehicle manufacturing industry.

Overall, China's spare parts manufacturing technology still belongs to the low-tech level. Some high-tech and core technologies are still in the hands of foreign manufacturers. The production of products such as shock absorbers, power steering, airbags, global positioning systems, and automatic transmissions is in an initial stage of development, and some are even in the starting stages.

PVC Non metallic LiquidConnector

PVC No-nmetallic Liquid Tight Connector descriptions:

1.No-nmetallic Liquid Tight Connector-Straight

2.UL list

3.Straight Nonmetallic liquid-tight connectors are used to terminate andseal Liquid -Tight Flexible Nonmetallic Type B Conduit to either an oil-tight, liquid-tight or rain-tight box or enclosure.Connectors can beused with tapered thread femaleentry or unthreaded knock-out using the provided sealingwasher and locknut.

4. Resists Salt Water, Weak Acids, Gasoline, Alcohol,Oil, Grease and Common Solvents

5. No Disassembly Required

6.Reusable

Pipe Fittings Sizes:

pvc pipe sizes chard id od inner diameter outer diameterAs mentioned in a previous blog post about PVC pipe outer diameter, PVC pipe and fittings use a nominal system for standard sizing. This is so all parts with the same size in their name will be compatible with each other. All 1" fittings will fit on 1" pipe, for example. That seems pretty straightforward, right? Well here's the confusing part: the outer diameter (OD) of PVC pipe is greater than the size in its name. That means that 1" PVC pipe will have an OD that is greater than 1", and a 1" PVC fitting will have an even larger OD than the pipe.

The most important thing when working with PVC pipe and fittings is the nominal size. A 1" fitting will fit on a 1" pipe, regardless of whether either one is schedule 40 or 80. So, while a 1" socket fitting has an opening wider than 1" across, it will fit on a 1" pipe because the OD of that pipe is also greater than 1".

More services we offer:

1 1/4 liquid tight conduit fittings,1 inch liquid tight conduit fittings,american fittings liquid tight,american fittings liquid tight connectors,liquid tight conduit connector 3/4

Timeplex Industrial Limited , https://www.timeplexhks.com